Frequently Asked Questions

General Self-Directed IRA Questions

Q: WHEN ARE STATEMENTS ISSUED?

A: Beginning in 2022, quarterly statements will be issued to all our IRA and ESA clients.

Q: WHY SHOULD I MAKE A CONTRIBUTION IF IT IS NOT TAX DEDUCTIBLE?

A: Non-deductible contributions grow tax free in a Roth IRA and tax deferred in a Traditional IRA. This tax-favored treatment usually makes even a non-deductible contribution a smart move.

Q: WHAT FORMS DO I NEED TO GET STARTED?

A: The forms needed to open an IRA are generally the Simplifier, Transfer or Rollover form and the Investment Direction form.

Q: WHAT IS THE DIFFERENCE BETWEEN THE COST BASIS AND MARKET VALUE?

A: Cost Basis is the amount paid for the assets, including any dealer fees or commissions.

The Market Value of precious metals shown on your statement reflects estimated bid values for each asset and not a firm price gauge to buy or sell through a dealer. Additionally, these estimated values do not include dealer mark-ups, discounts, or commissions. Current price estimations for bullion and proof products can be obtained from various sources including your dealer.

The Market Value of bonds includes the principle amount for simple interest bonds or principle plus compound interest for compound interest bonds.

The Market Value of loans funds, mutual funds, stocks, foreign assets, etc. may be updated monthly, quarterly, semi-annual, or annually based on the individual asset.

Q: MY STATEMENT SHOWS A MARKET VALUE LESS THAN I INVESTED.

A: The fair market value we provide is a bid price or wholesale price used for tax reporting purposes. You could reasonably expect to sell for at least this amount. GoldStar updates this value every two weeks. Any fees or commission paid to your dealer may have been included in your purchase price. Please call your dealer for real-time sale pricing and any fees or commission paid.

Q: CAN I TAKE POSSESSION OF IRA ASSETS?

A: No, all IRA assets must remain within the custody of a custodian or trustee of the IRA. Precious Metals must be stored in an IRS approved depository. You may take a distribution of assets in your IRA, which is a taxable event reported to the IRS.

Q: WHAT TAX FORMS CAN I EXPECT TO RECEIVE FROM GOLDSTAR TRUST COMPANY?

A: IRS 1099R: reports taxable distributions from an IRA to the IRS and the account holder. The 1099R is mailed by January 31st each year and reports all distributions from the IRA for the prior calendar year. Box 7 “Distribution code” describes the nature of the distribution. The least restrictive code is “7”; for normal, penalty free distributions of a Traditional IRA to the qualified owner. Roth conversions are also reported on the 1099R.

IRS 1099OID: reports taxable compound interest (CI) accrued during the tax year, but not paid to the client.

IRS 1099INT: reports taxable interest paid on simple interest (SI) bonds

IRS 5498: is sent out after April 15th (tax deadline) and before May 31st. This form reports the December 31st Fair Market Value and contributions for the prior-year. The IRS Form 5498 is sent out after April 15th since contributions to an IRA can be applied (postmarked) through April 15th. IRS regulations require GoldStar to send the forms to the client and the IRS. A 5498 is informational and not required to file a tax return. Recharacterization, RMD required distributions, and rollovers are also reported on the 5498.

Real Estate Self-Directed IRA Questions

Q: Who is a disqualified person?

A: A disqualified person is any person who is in a position to exercise substantial influence over the affairs of the applicable tax-exempt organization at any time during the lookback period. It is not necessary that the person actually exercise substantial influence, only that the person be in a position to do so. Brothers, sisters, aunts, uncles, cousins, step-siblings, mothers-in-law, fathers-in-law and friends are not treated as disqualified persons.

Examples of Disqualified persons:

- IRA holder and their spouse

- Lineal descendants: IRA holder’s children, grandchildren and their spouses

- Lineal ascendants: IRA holder’s parents and grandparents

- Anyone that provides services to the IRA: Investment advisors, managers and fiduciaries

- Any corporation, partnership, trust, or estate in which disqualified persons have a 50% or greater interest

Q: Am I required to obtain a property manager?

A: GoldStar requires you to obtain a property manager for income producing properties. The property manager will need to sign our Property Manager Agreement.

Q: As the account owner can I be the property manager?

A: No, as the account owner you cannot act as the property manager as this could be considered a prohibited transaction.

Q: How should the contract for the property be titled?

A: Since the IRA account is the owner of the property the contract must be titled as GoldStar Trust Co. FBO (IRA Owner Name), IRA. As the account owner, you will initial and date all documents as read and approved. GoldStar will then sign on behalf of the IRA.

Q: How should expenses for the property be handled?

A: Any and all expenses must be paid out of the IRA.

Examples of expenses:

- Utilities

- Repairs

- Taxes

- Mortgage Payments

- Escrow Funds

- Property Insurance

Q: How do I direct GoldStar to pay the expenses?

A: For any expenses not paid by the property manager please complete the Payment Authorization Form.

Q: How should income for the property be handled?

A: All income that the property generates must be submitted to GoldStar to be posted into the IRA. Rent checks should be made payable to GoldStar Trust Co. FBO (IRA Owner Name), IRA. Please make sure to include the Rental Coupon with the rent check.

Q: Can my IRA borrow money to purchase the investment property?

A: Yes, through a non-recourse loan.

Q: What is a non-recourse loan?

A: A non-recourse loan is a loan agreement under which the collateral securing a loan is the ultimate source of repayment, and the lender cannot hold the borrower personally liable in the event of a default. A non-recourse loan allows a borrower to finance the purchase of the real estate property. GoldStar must sign the documents on behalf of the IRA. Titling must be GoldStar Trust Company FBO: Client Name IRA.

Q: How can I obtain a non-recourse loan?

A: Not all banks offer non-recourse loans. Here are a couple of banks that offer non-recourse loans, however you are free to research other lenders.

North American Savings Bank – 866.735.6272

First Western Savings Bank – 800.908.8845

Q: What is Unrelated debt financed income (UDFI)?

A: UDFI applies to the gains received by an IRA that are attributable to debt. IRC Section 514 When a non-recourse loan is obtained and used in connection with an IRA purchase; it may subject the IRA to unrelated debt financed income tax. This tax must be paid by the IRA and is determined by the largest amount of debt carried by the plan for the previous 12 months. The IRA, not your personally, is responsible for paying any UBIT tax liability. GoldStar does not offer any tax advice and recommends that you consult with your tax professional.

Q: What is Unrelated Business Income Tax (UBIT)?

UBIT applies to ordinary income received by an IRA if the IRA generates gross income of $1,000 or more during the tax year. IRC Section 511 “UBIT tax is due from an ordinary income producing business when such business is a flow through company not paying corporate tax.” The Self Directed IRA Handbook – Mat Sorensen

There are three common events that may trigger UBIT.

- The IRA buys LLC ownership in businesses that provide goods or services (e.g. restaurant, tech-company, business selling services or goods). UBIT may apply if the LLC is structured as a pass-thru entity for taxes that does not pay corporate taxes.

- The IRA invests in real estate investment assets that do not result in investment income. An example would be a real estate development or buying and selling a large number of short-term real estate “flips”. This will cause the assets to be considered as inventory versus investment assets and may result in taxable income.

- When an IRA buys real estate with a non-recourse loan. A non-recourse loan can be obtained when the IRA owner does not have sufficient IRA funds to make a real estate purchase.

Q: What types of real estate may I invest in within my IRA? Are there any restrictions?

A: Single Family, multi-family, commercial, and raw land can be held within an IRA here at GoldStar. International real estate assets are not permitted to be held within in the IRA at GoldStar.

Q: How do I invest in real estate at GoldStar?

A: If you do not have an established IRA with Goldstar, please click on the corresponding account application link below. We have created the following kits so that all forms necessary to establish and fund your IRA can be found in one place. To rollover your 401k or other qualified plan please contact your current custodian for their requirements as they do not always accept our paperwork.

Traditional IRA Real Estate Investment Kit

Roth IRA Real Estate Investment Kit

After your account has been funded you are now ready to make your purchase. Once you have found a real estate investment follow the Real Estate IRA Checklist to ensure that your purchase goes smoothly.

Q: Appraisal / Comparative Market Analysis

A: There are two types of acceptable valuation methods; Formal appraisal and Comparative Market Analysis (“CMA”). A comparative Market Analysis should be completed by a local Real Estate Broker (“Valuation Agent”).

Formal appraisals are required for the following types of transactions:

- Roth Conversion or Recharacterization

- Required Minimum Distribution (“RMD”) RMD is being taken.

- Distribution In Kind – the account owner initiates a distribution in-kind from the IRA to his/her self.

CMA appraisals are required for the following types of transactions:

- Annual valuations – required for existing real estate held in an IRA at Goldstar Trust. The CMA is required by January 10 of each year.

Paper Statement Questions

Q: Why am I being charged a paper statement fee?

A: The electronic delivery method was not elected prior to October 1, 2021.

Q: What fees are associated with paper statements vs. electronic statements?

A: There is a $25 annual fee associated with paper statements. During 2021, the fee was pro-rated for $6.25 per statement. Going forward the paper statement fee will not be pro-rated. There is a $10 reprint fee per request for a paper statement.

Q: How can I avoid the paper statement fee?

A: Sign up for Electronic Delivery through your online account.

i. Go to https://www.goldstartrust.com

ii. Click on Login

iii. New User

1. Click the Register Link

2. Follow the prompts for E-Statement election

iv. Existing Users

1. Login as normal with Username and Password

2. Go to My Profile by selecting the silhouette in the upper right-hand corner

3. Create a Security Phrase if you haven’t done so already

4. Select a Statement Delivery option (Paper or E-signature)

5. Scroll to accept the E-disclosure

For existing accounts, the statement election must be made by March 31, 2022 to avoid the paper statement fee of $25 that will be assessed on June 30, 2022. For new accounts, the statement election must be made within 30 days of account opening. Per our fee schedule, annual fees are not pro-rated.

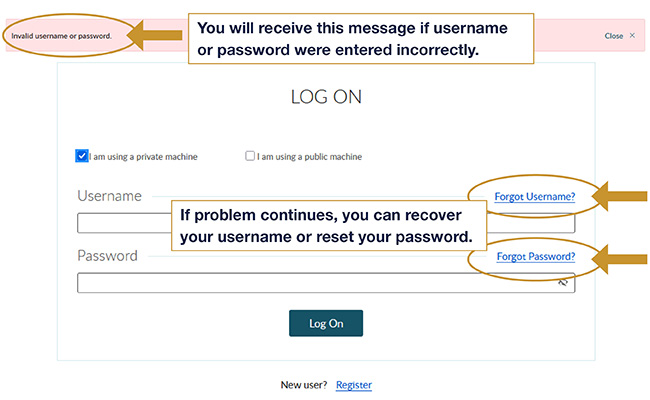

Q: Can I make the election via phone or email through a GoldStar representative?

A: No, the election can only be made after the electronic delivery disclosure has been accepted and approved through the online portal. GoldStar representatives cannot make this election on your behalf.

Q: How many statements do I get a year?

A: Beginning in 2022, GoldStar will be providing statements quarterly.

Q: Will I receive my statements through E-mail or through the Online Portal?

A: Statements can be retrieved through the Online Portal Statement and Documents Page. The statements and tax documents will not be sent through email.

Q: How do I access Statements and Tax Documents once I have an online account/login?

A: Login as normal and select Statement and Documents Tab. You may have to adjust your filter options and time frames to see the most current time frames.

Q: Can multiple accounts share an e-mail address?

A: No, each individual client will need a unique email to sign up for e-statements. To update your email address with GoldStar please complete and submit our Account Update Request Form. You may submit the form by email to info@goldstartrust.com or by fax at 806.655.2490.

Statement Questions

Q: Why do the statements look different?

A: Our system upgrade allowed us to enhance our statements.

Q: What is the asset allocation section telling me?

A: This section provides a graphic of the breakdown of assets, including cash, held within your account.

Q: The activity summary section values don’t add up, why not?

A: This section just highlights certain transactions that took place and is not a full accounting of what happened on the account.

Q: I recently made a purchase, why isn’t it showing?

A: Depending on the date of your purchase it may not show, as these statements only include transaction made from 07/1/2019 through 12/31/2019.

Q: What does cost basis mean?

A: This is the amount that was originally paid for your asset.

Q: Why is there a section for ‘tax year’ if it isn’t always populated?

A: The ‘tax year’ section is to show when transactions are for prior years. An example would be when a client makes a prior year contribution to their Traditional IRA.

Q: What does receive free mean?

A: When you see the term “receive free” it means that a transfer in of an asset as occurred or that the principal increased on an asset. This will cause the cost basis within the asset to show $0.00 as no cash actually posted into the IRA.

Q: What does free deliver mean?

A: When you see the term “free deliver” it means that a transfer out of an asset as occurred or that the principal decreased on an asset.

Q: What does Fee Debit Auto Pay mean?

A: This description means that the fee was paid from the available cash in the account.

Q: What does balance forward mean?

A: Balance forward means that a previously assessed fee is still outstanding and is being carried forward.

Q: The activity summary section shows a line item of ‘sales’ what does that mean?

A: This line item appears if a transaction was entered without the proper cost basis. The cost basis could be incorrect or missing altogether.

Q: I have past due fees, how do I pay them?

A: Simply click on the PAY YOUR FEES tab in the top navigation bar and select your preferred option for paying the fees.

Q: Can I make a contribution to my IRA?

A: Yes, contributions can be made via check. Checks should be made payable to GoldStar Trust Company FBO: (client name) and include the tax year the contribution should be applied. Forms are available on our FORMS page under FUNDING.

Q: Why is my SEP/SIMPLE contribution showing the incorrect year?

A: Per IRS regulations GoldStar must post the SEP/SIMPLE contribution in the year it is received.

Q: How do I find the privacy policy?

A: The privacy policy is available from the footer of any page of our website. Click here to view it now.

Q: How do you figure the unrealized gain/loss?

A: To figure the unrealized gain/loss you will take the market value and subtract the cost basis.

Q: Can I view my statement(s) online?

A: Yes, statements will be made available through the online platform within 30 days of the ending statement date.